The VA funding fee is part of the process of getting a VA loan. Here we provide a VA funding fee chart so if you are in the process of trying to get one of these loan guarantees, you will have a good idea of what you may need to pay. There are some exemptions – service members and veterans who don’t have to pay the fee – and different rates apply depending on the type of loan. As you make your calculations for your VA loan to purchase a home, or refinance your mortgage, include this fee in your list of expenses.

Here’s a look at the ins and outs of the fee.

What is the VA Funding Fee?

VA Loan Fees are something you pay during your closing costs, so it does not necessarily come out of pocket (more on that below). This fee does pay to support the VA Loan system, which insures and guarantees loans for armed forces service people, veterans and surviving spouses. That’s important because the VA Home Loan program has been responsible for helping more than 25 million veterans and active duty armed forces personnel since it began, and it helped 1.2 million heroes in 2020 alone.

That’s the good news/bad news: you will be required to pay the fee, but it helps keep the VA Loan system alive for veterans as well as active duty military personnel.

The one-time fee kicks in at different levels for different loans offered by the VA. If you thought the U.S. Department of Veterans Affairs only offered one kind of loan, you should learn about the whole range of options that help you buy a home and refinance your mortgage after you’ve had your home for some time.

Purchase

When you purchase a home using the VA loan system, the funding fee can range between 2.3 – 3.6 percent of the loan amount. If you are looking at homes in the $300,000 range, that means your VA funding fee could be between $6,900 and $10,800.

VA IRRRL

The VA Interest Rate Reduction Refinance Loan may not be on your radar, but it should be. This is a refinance loan you can use to reduce the interest you pay on your mortgage. That typically becomes an option if interest rates are falling, but if you can successfully refinance it can reduce your monthly payment in the short term, AND your overall mortgage payments in the long term.

This is known as a streamline refinance by the VA. It requires a lot less documentation, fewer requirements and less stress overall. It is also a fast refinance and can usually be in place in about 30 days. Consequently, the VA loan funding fee for this process is quite a bit lower than any of the other loans in the VA system (see chart below).

This option is only open to those who already have a VA mortgage.

VA Cash Out Refinance

This is another refinance option from the VA, but this lets you refinance your mortgage and turn the equity you’ve developed in the property into cash. You can use this cash to repair your home, renovate it, install energy efficient elements, pursue your education and take care of emergencies (for example, medical bills).

Since the VA Cash Out Refinance is not streamlined and very much like a typical refinance with all the rules and documents, you will pay a higher funding fee than other loan options (more like you would pay for a typical VA Purchase Loan.

This option is open to VA Loan holders and conventional mortgage holders who qualify for a VA loan but may have missed it the first time out. That ability to convert a conventional loan into a VA mortgage, and get cash back, makes this a very attractive option under the right circumstances.

Native American Direct Loan

If you’re a veteran, and either you or your spouse is Native American, you could be eligible for the NADL. These loans let you buy, build or improve a property on federal trust land. If you qualify, you can also use this loan to refinance your current mortgage. With the NADL, you will pay the VA funding fee, but at a much lower funding fee than other VA Loans.

The VA Funding Fee Breakdown

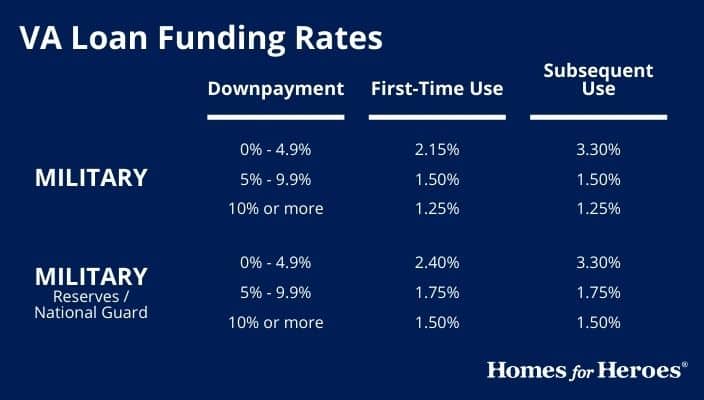

The big question around the VA Funding Fee is “how much?” as in how much will you pay in your circumstances. As with most matters involving either the federal government or the real estate industry, the answer gets more complicated as you get more specific. The chart below shows VA Funding Fee rates and should help you sort out what you might be paying.

VA Funding Fee Chart

There are Funding Fee Exemptions

While the VA Funding Fee is pretty universal among the loans provided by the organizations, there are some notable exceptions to the fee, especially for disabled veterans. If you qualify for any of these, you may get your VA Funding Fee waived.

- Are you a veteran who receives compensation for a service-related disability?

- Are you eligible for service-connected disability pay but receiving retirement or active duty pay instead?

- Are you the surviving spouse of a veteran who died in service or from a service-related disability?

- Are you an active-duty service member who has been awarded the Purple Heart?

- Do you have a memorandum rating saying you are eligible for compensation based on pre-discharge claim?

If you think you may be exempt from the funding fee, but aren’t sure, you should probably contact the VA and talk to someone. If you pay the funding fee and later realize that you qualify for an exemption (if, for example, the paperwork didn’t come through in time), you can get a VA Funding Fee refund.

If you’ve already got your Certificate of Eligibility, which is a key document in almost every VA loan process, it probably lists whether you have an exemption to the VA Funding Fee. It could also be part of your Verification of VA Benefits form (also called the VA Funding Fee Exemption Form).

Alternative Ways to Pay It

It’s important to remember that, while the VA will insure and guarantee the loans mentioned here, the actual loans themselves come from private lenders. They are responsible for collecting the funding fee at closing and sending it to the VA. There are three ways to pay the funding fee:

- Pay it out-of-pocket at closing.

- In most cases, veterans and service members choose to roll the funding fee into the mortgage loan. This will save you money up front, but it will increase the total loan amount and the interest you pay over the life of the loan.

- You could negotiate with the seller of the house to have them pay the funding fee.

The VA Funding Fee may seem a costly obstacle to a VA Loan benefit, but you need to weigh the fee against all the financial advantages of these government-backed loans. Those cost savings include: no down payment, no private mortgage insurance, a lower interest rate and more.

There is a lot of focus on the Department of Veterans Affairs when it comes to finding a mortgage through their system, but your mortgage lenders are a very important player in the process. Your relationship with your mortgage specialist will smooth out a lot of bumps along the way. That’s where Homes for Heroes can help. Whether you are buying a home or refinancing your mortgage, our network of mortgage specialists can help you every step of the way.

If you are hoping to buy a house and use the VA home loan benefit, Homes for Heroes can connect you with a real estate agent and loan officer – a whole team of real estate and mortgage professionals who can help you along the way. At the end of the process, when you close, we will give you a Hero Rewards check to thank you for your service. The average rewards check is about $3,000, and you can use that for appliances, furniture, renovations…whatever you want.

If you are only refinancing, let Homes for Heroes help you find the right private lender. Our network of mortgage specialists want to help active duty military personnel and eligible veterans find the best deal for their long-term and short-term financial lives.

Estimate Your Savings

Learn how much you could save on your home purchase. Adjust the slider to see potential savings when you buy with a Homes for Heroes real estate and mortgage specialist. This is an estimate. Your actual savings may vary.